I view this text as very preliminary. I will take a long look at it again once I have the rest of the book put into place. My plan is that the book was supposed to be a short report, and it may be that I am near the end of overall text structure. I then need to fill in more details - data from other countries, more references - but I will do that once all the sections are assembled. There is no point tracking down data and references for a section that ends up getting deleted completely.

The usual convention is for inflation to refer to the cost of goods and services – things people buy. From a macroeconomic standpoint, a good deal of “inflation” discussions are about another phenomenon – wage growth.

From the perspective of most individuals, getting a pay increase is a good thing. An increase in the price of goods and services means you can buy less stuff, and that is viewed as a bad thing. This fits the framing that inflation is bad.

Once we start looking at the macroeconomy, the emphasis starts to shift. The labour market is watched intensely.

Wages are Domestic, Prices Often International

The bond market reacts to the interest rate policy decisions of the central bank, and modern central banks are generally mandated to control inflation. That said, they have very little control over many key prices, such as oil prices.

Oil prices are set in international markets, driven by both private firms and state actors. If oil prices increase, rate hikes by the Bank of Canada would do very little to tame them. Even rate hikes by the U.S. Federal Reserve might do very little to oil prices if the reason for the price increase is either a supply constriction or a demand increase elsewhere in the world.

Policymakers need to focus on what they can feasibly control, which is the domestic economy. Wages represent one of the most important domestic prices (the price of labour).

(As an aside, one could argue that policymakers could adjust the level of the currency to counter-act rising international prices. Since the developed economies generally let their currencies float, this is not possible. But even if the currency were controlled, it is not necessarily a good idea to let your currency increase in value in response to an oil price spike if you are not a major oil exporter. Rising energy costs displace other spending, and so there is a demand shortfall in the developed countries that import oil. This means that your exporters would face a double whammy – falling external demand, as well as a loss of competitiveness from currency appreciation.)

Relationship Between Wages And CPI

From the perspective of mainstream theory or post-Keynesian theory, we expect to see a relationship between wage growth and inflation. However, there are considerable differences of opinion regarding the exact mechanisms involved. So long as we focus on prices determined by domestic macro factors, we generally see a relationship. In a country where imported goods or non-processed foods represent a large part of the CPI basket, then there can be large divergences between wage growth and CPI inflation.

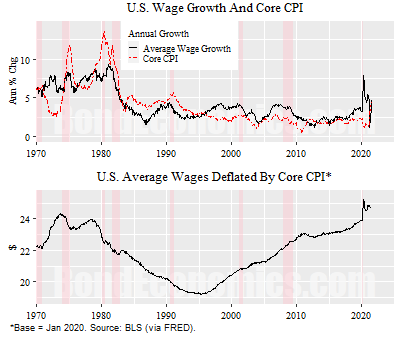

When we look at the data, we typically see that wage growth and CPI inflation move together. The chart above shows the U.S. experience, comparing average hourly wages to the core CPI. The top panel shows growth rates and see that they tend to rise and fall together – but not at the exact same rate. (The pandemic caused an unusual spike in 2020 – lower-wage workers were disproportionately stopped from working by health directives, and so the mix of workers shifted towards higher-wage workers, raising the average.) I used core inflation to demonstrate how it is smooth, very much like the wage growth series.

The bottom panel shows the ratio of wages to core inflation. Using core inflation in the ratio is admittedly an unusual choice – we normally want to do the ratio to headline. I kept it with core CPI so that it is directly comparable with the previous panel. Since the average hourly wages are in dollars while the CPI index is a number without dimensions, the ratio is arbitrary. I set the scaling of the ratio so that the displayed series equals the original value in January 2020, which is often described as using a January 2020 baseline. We can think of the series as average wages in 2020 dollars (keeping in mind that I used core CPI). We see that there are smooth trends – falling in the 1980s, and then recovering in the mid-1990s until just after the Financial Crisis of 2008.

So long as we lop out oil prices – largely driven by global factors after the 1990s – we can say that there is a relationship between wage growth and CPI inflation.

So long as we keep in mind the domestic/global distinction, we can see that CPI and wages represent different segments of a wider notion of “domestic prices.” I will often refer to this wider concept as the “price level” – a generic notion of prices that includes all the major components of the prices of current goods and services, which includes wage measures and producer prices as well as the CPI. However, I do not include asset prices within this concept, as I discuss further in Chapter 4.

(As an aside, the bottom panel could be used to discuss the standard of living of workers over time. However, if the (core) CPI systematically deviates from the true “cost of living,” then the readings for the “real wage” are not comparable over the decades. If we accept the common view among economists that the CPI overstates the “cost of living,” then wages should have a rising trend over time that is not apparent in the figure.)

Lots of Theories

There is a long history of arguing that conditions in the labour market determine the inflationary trends in the economy. In economic commentary, you will see many references to concepts like the Phillips Curve, the non-accelerating inflation rate of unemployment – more normally referred to by its acronym NAIRU.

If we ignore the details, we could paraphrase these ideas as: if the labour market gets “tighter” (or “overheated”), wages and then CPI inflation will rise with a delay (“lag” in economist-speak).

If we stick to generalities, this largely represents my beliefs about the causes of inflation (with various exceptions). However, the problem is getting more specific. As soon as we try to come up with a mathematical model that links observed labour market data to inflation, the models sort-of work until they do not. The determination of inflation is complicated.

(Since many of my readers are fans of Modern Monetary Theory, I would note that my comments here largely refer to existing institutional arrangements. The argument is that the introduction of a Job Guarantee programme would help stabilise wages and thus the price level. I discuss this in my book Modern Monetary Theory and the Recovery, such as in Section 4.3. However, we cannot point to historical data to demonstrate this conclusively yet.)

Why There Should be a Link

To what extent workers have cost of living adjustments (COLAs) in their bargaining agreements, a rise in CPI inflation will tend to raise wages. This certainly was a factor in the 1970s, when private sector unions were relatively more powerful than now. Even in their absence, every firm that has employees has wages embedded in their cost of doing business. There are two fighting flavours of theories to link wage costs to output prices.

The mainstream view is that firms set wages based on the value of the output of the “worker at the margin”: if output prices rise, they can pay more.

The post-Keynesian view is that firms set prices as a markup over the cost of production. So if worker’s wages go up, the cost of production goes up, and so firms want to raise prices to compensate.

I lean towards the post-Keynesian view, but both views point in the same direction. If wage costs rise, then we should expect the cost of domestically produced goods and services to also rise (sooner or later). This explains why central bankers and bond market participants pay a great deal of attention to labour market data, instead of obsessing about the price increases of Crunchy Cheese Treats in the snack section of your local grocery store. Admittedly, they tended to analyse the data incorrectly, but nobody is perfect.

The relationship between wages and CPI inflation is not the simple case of one being a constant ratio to another (which marginal theories might suggest). Wages are a cost of doing business, and if they go up without output prices rising, profits fall. This leads to the post-Keynesian conflict theory of inflation. Workers and firms each attempt to increase their income share, and wages and output prices increase to accommodate this.

It is a basic accounting fact that the ratio of wages to output prices determines profit margins, and that ratio is not constant. The only real debate is around whether we can make useful predictions using this observation. Since I do not want to get into theoretical disputes within this introductory text, I will just point the reader to Chapter 17 of Macroeconomics by Mitchell, Wray, and Watts for more details.

Output Has to Be Bought

The general demise of cost-of-living adjustments means that the psychological link between CPI inflation and wage growth has faded. To a certain extent, there is a fear that inflation just destroys workers’ standards of living. This is certainly what it feels like from the perspective of an individual.

From a macroeconomic perspective, we see that it is harder to de-link the two. Produced output has to be bought, or else it piles up as unsold inventory.

For example, imagine that the price of goods and services suddenly rose by 10%, while wages did not respond. Unless workers suddenly dip into their savings to make up for this, the implication is that workers can buy 10% less stuff. The most likely outcome is that this would trigger a recession (albeit with an unlikely exception that I will return to). Pricing power of firms normally softens in recessions, counter-acting the previous price jump. Very simply, raising prices of goods and services without rising wages to purchase them is difficult.

That said, we can see such outcomes in the real world, which are typically the result of a currency collapse or a supply disruption (e.g., a failed harvest). If the price of a critical import spike in price, a country faces a drop in the standard of living. Such episodes are common, but currently less of an issue for most developed economies. As firms get used to operating in a floating currency regime, they become less sensitive to foreign exchange volatility. Also, developed countries feature less food inflation swings. the industrial food sector has more reliable yields, a diversified set of suppliers all over the globe, and the layers of processing between the raw food inputs and the output “food product” means that large changes to raw food prices only have a limited impact on final prices in the grocery store/

This explains why the phrase “price and wage spiral” is commonly used in the discussion of inflation: wages generally need to rise in order to purchase goods that are rising in price.

As a final theoretical point, we can imagine a possibility where output prices rise but wages are unchanged – the owners of capital spend the increased profits to make up for the loss of purchasing power of workers. Although this happens to a certain extent, the extent of this effect are limited. Very simply, rich people are not going to run out and buy all the Crunchy Cheese Snacks that workers cannot afford to purchase.

Productivity

The conflict theory might suggest that workers and employers are fighting over a fixed size income pie. This is essentially true in the short term, but over the longer term, the pie itself is growing. This means that both wages and profits can grow faster than the rate of inflation.

The reason that the pie is growing is chalked up under the term productivity. The output per hour of workers has tended to increase. This can largely be attributed to technology in its various forms, in particular the ability to harness concentrated energy, and increased agricultural yields. The increase in agricultural output has allowed developed societies to transition from mainly rural to mainly urban. However, the increase in productivity can be the result of more efficient institutional structures (possibly aided by new information processing technology).

Historically, productivity growth has been high, and there is a common assumption that this will continue going forward, because it is somehow an inherent property of industrial capitalism. From the perspective of Peak Oil, this is a dangerous assumption. The harnessing of the concentrated energy in fossil fuel sources went hand-in-hand with the rise of industrial capitalism. That era is coming to an end, either due to environmental concerns or resource depletion. Industrial societies may be able to innovate away from fossil fuel usage, but their ability to do so is still largely untested.

Concluding Remarks

Average wages will not rise at exactly the same pace as goods inflation. Nevertheless, there is a strong linkage between domestic prices and wages if we are looking at what is happening within a business cycle. This has the result that labour market data is the most closely followed set of macro data.

References and Further Reading

Macroeconomics, by William Mitchell, L. Randall Wray, and Martin Watts. Red Globe Press, 2019. ISBN: 978-1-137-61066-9

No comments:

Post a Comment

Note: Posts are manually moderated, with a varying delay. Some disappear.

The comment section here is largely dead. My Substack or Twitter are better places to have a conversation.

Given that this is largely a backup way to reach me, I am going to reject posts that annoy me. Please post lengthy essays elsewhere.