It may very well be that the bond bears will be ultimately vindicated. However, the rule of thumb from previous cycles is that you do not want to be sitting in short positions too far in advance of the rate hike cycle. Negative carry adds up if you are stuck in a position for three years or more.

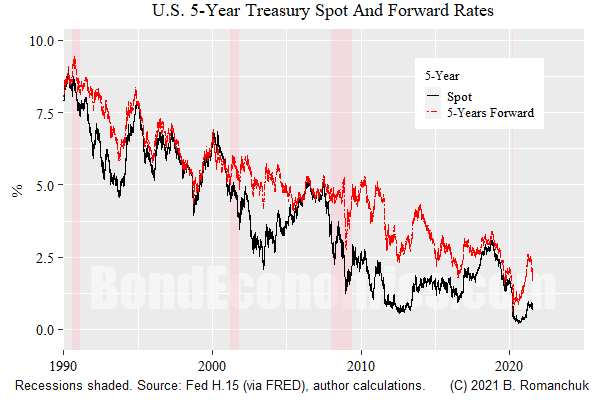

The chart above shows what is driving the benchmark 10-year yield, by decomposing it into a spot and forward component (each of 5-years length).

The spot 5-year rate has risen from ultra-low levels, but is stuck near the lows of the previous cycle. This is not exactly unexpected if you expect that the Fed will be on hold for years to come. If you think the Fed will start hiking rates relatively soon, shorting the front end is probably the way to go. Why worry about term premia moving against you, when you have a nice clean shorting opportunity? Very simply, if you think rate hikes are coming within a year or so, there is not a whole lot of thinking involved behind the duration call.

The 5-year rate 5-years forward has also risen, but is still lower than it was last cycle. If you want to make a valuation case against long-term rates, this is what you pound the table about.

The bear valuation case is extremely well known. Deficits! Fiscal sustainability! Money Printing! The FED! Bitcoin (why not?)! Inflation is really 8%! Etc.

I do not have a lot of sympathy for the bond bears, mainly on the grounds that the individuals involved have been wrong in the same way for a long time, possibly decades. (As a recovering secular bond bull, my memory for terrible bond bear calls is long.) That said, I can see how someone could construct a more plausible case for inflation than last cycle (where there was no case whatsoever). As such, even though most of these bond bears have been repeatedly wrong, perhaps they could be bailed out this time.

Conversely, the case to be cautious about valuations is to compare the forward 5-year rate versus historical spot rates. We see that is above the level of most of last cycle. Although having a larger valuation cushion would be nice, the level is not outright crazy.

Since I am not offering investment advice, I will not waste my readers’ time by digging further. I just want to highlight the possibility of the boring outcome: a trading range until we are closer to the first rate hike.

Other Work Comments…

I have been concentrating on my agent-based model project. I am in the process of cleaning up code (“refactoring”), which does not generate a whole lot of interesting insights into economics. However, I want to get through that while the code is still fresh. Once the code is cleaned up, it will be easier to dip in and out of the project.

As for my inflation manuscript, it is up to 15,000 words, which is a good chunk of its target size. Since the book is mainly a description of what inflation is, and not a discussion of theories about inflation, it makes sense to keep it short. (I announce that I intend to keep all my reports short, and then they all overshoot targets.)

I am otherwise in the process of recharging my batteries, and probably have relatively low output for next few weeks.

This link on financial services was very useful for my search. If you don't know about the Who Can Invest in Private Markets? then ADDX financial services helps you.

ReplyDeleteThis comment has been removed by a blog administrator.

ReplyDelete